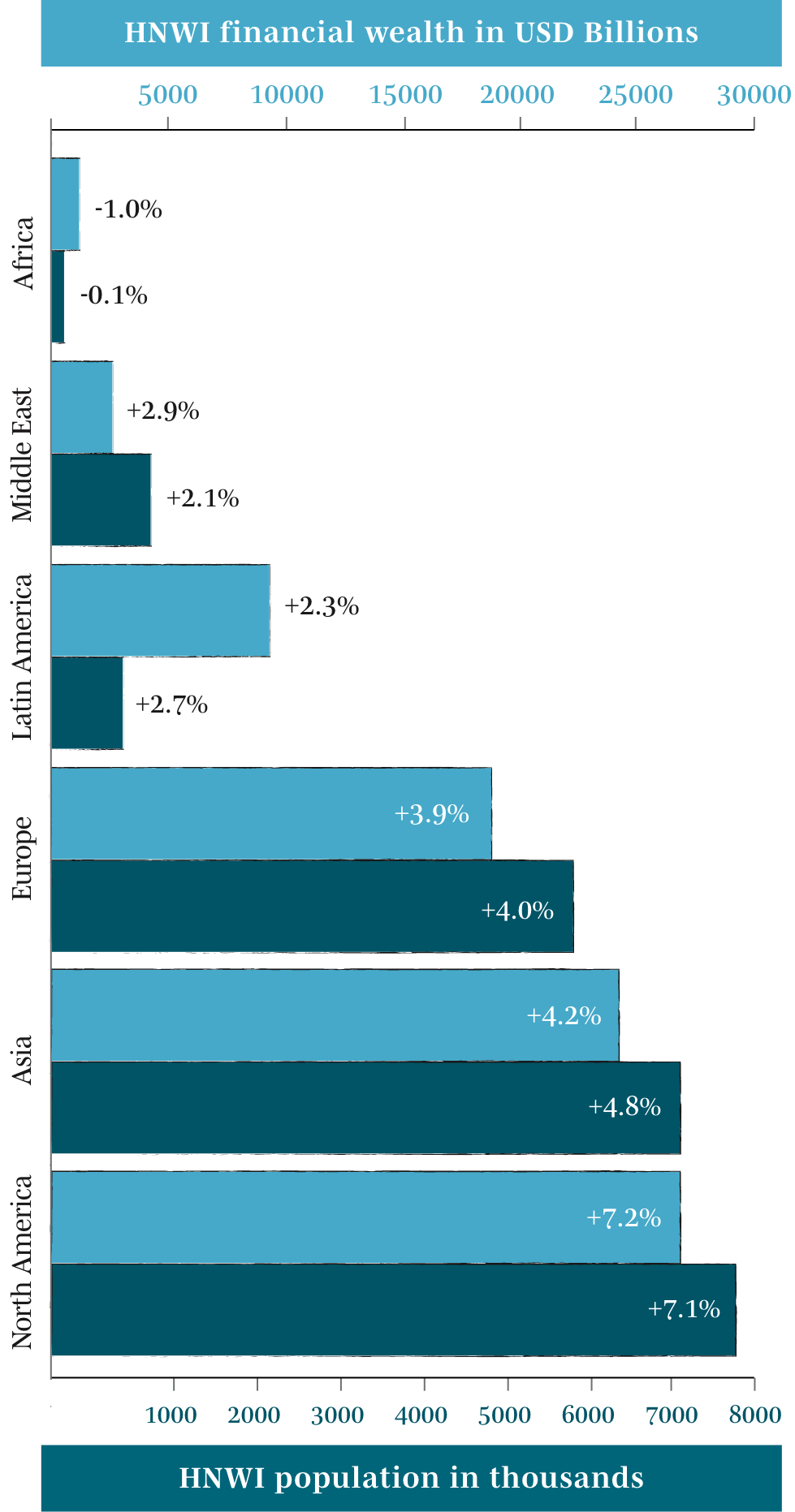

In 2022, a decline in global wealth1 and ongoing geopolitical uncertainty led to a 3.3 per cent drop in the number of high-net worth individuals, known as HNWIs in industry parlance.2 However, recent data points to a recovery: Capgemini’s World Wealth Report 2024 shows that an improved global economic outlook drove HNWI numbers and wealth to record highs in 2023.3 The global HNWI population rose by 5.1 per cent to reach 22.8mn and continues to grow despite market volatility.

HNWI Growth Globally in 2023

Source: Capgemini Research Institute for Financial Services Analysis, 2024.

Today’s deeply unsettled times are marked by escalating global conflicts, rising energy prices, extreme weather driven by climate change and an unstable geopolitical landscape – all factors contributing to market instability. While such flux may present bold opportunities, risk-averse HNWIs are increasingly scrutinising their portfolios. Among the available options, a range of life insurance products could help mitigate risks to personal wealth.

As senior portfolio manager for asset allocation at Manulife Investment Management Asia, Marc Franklin is aware of these complexities and recommend clients on strategies to protect their assets.

“There are a number of risks to be cognisant of as investors head into 2025,” says Franklin. “Among them, China’s moderating growth and a slowing global economy are two of the most critical for Singapore’s HNWIs.”

“There are a number of risks to be cognisant of as investors head into 2025. Among them, China’s moderating growth and a slowing global economy are two of the most critical for Singapore’s HNWIs.”

Marc Franklin

Senior portfolio manager, Asset Allocation for Manulife Investment Management Asia

As Asia’s largest economy, China is an important driver for Singapore’s economic landscape.4 However, Franklin shares that “listed companies directly or indirectly reliant on China’s economy are likely to see ongoing volatility in their growth paths”. And while China’s offshore credit markets have historically been a source of higher-yielding investment for HNWIs,5 the structural headwinds impacting China’s real-estate sector and wider economy raise concerns. “HNWIs need to factor in a higher default or credit stress risk in their assessment of what represents ‘value’ from a yield-to-maturity perspective,” cautions Franklin.

Meanwhile, the global economic outlook remains uncertain.6 Interest rates are falling in most major economies, and with them, bond yields are diminishing.7 This raises the question of how HNWIs can continue to generate mid-single-digit income returns without taking excessive risk. “A slowing global economy necessitates that HNWIs adopt a more selective approach to how they allocate their capital and investments,” advises Franklin. In such conditions, fortunes often sharply diverge between strong, resilient companies and economies, and those that are weak or speculative.

“A slowing global economy necessitates that HNWIs adopt a more selective approach to how they allocate their capital and investments.”

Marc Franklin

Senior portfolio manager, Asset Allocation for Manulife Investment Management Asia

For Franklin, this underscores the urgent need for extensive due diligence and fundamental research in investment decisions. He recommends HNWIs to “pivot towards asset classes and specific investments that are well placed to emerge in a strong position from any prolonged or sharp slowdown or period of volatility”. While some HNWIs may rely on personal insights, Franklin notes that many risk-averse investors prefer to rely on active fund managers.

Of course, although market volatility can seem alarming, it remains a regular and normal feature of global economics that investors can usually weather. For many, it’s a timely reminder to add or enhance life insurance in their personal portfolios to help mitigate financial risks and build confidence in their family’s future.

For example, Indexed Income and Indexed Universal Life Insurance products generally offer downturn protection. While the credited interest is linked to the performance of the S&P 500 index, a minimum floor rate safeguards the cash value against significant market downturns. This is achieved “by offering protection against significant negative returns during market downturns while also providing the potential for higher returns tied to market performance”, explains Thomas Lee, chief product officer at Manulife Singapore. “Indexed income products deliver a balanced solution for clients seeking both stability and potential growth in their portfolios.”

“Indexed income products deliver a balanced solution for clients seeking both stability and potential growth in their portfolios.”

Thomas Lee

Chief product officer at Manulife Singapore

In line with Franklin’s point on closer investment management, some life insurance products are designed for clients to self-manage the underlying portfolio. This approach enables them to cherry-pick investments and build a legacy using existing assets such as equities and bonds. The death benefit of such life insurance is a guaranteed lump sum paid to beneficiaries, helping them cover immediate expenses, settle debts and distribute the estate fairly without delays or the costs associated with probate. In a volatile market, this reassurance can be invaluable.

However, 2025 also brings positive prospects. “We expect a number of secular themes to continue to play out in 2025, offering compelling investment opportunities,” says Franklin. “These include geopolitical tensions driving investment in cybersecurity and a combination of climate mandates and energy security fears driving investment in nuclear power.” The flexibility and liquidity of some life insurance products allow even risk-averse HNWIs to access cash at critical moments and capitalise on market opportunities as they arise.

The cyber security market revenue is expected to show an annual growth rate (CAGR 2024-2029) of 7.92%, resulting in a market volume of US$271.90bn by 2029.

Source: Statista8

Everyone has a different appetite for risk, but having a measure of certainty during uncertain times is always reassuring. “Incorporating life insurance into a portfolio allows HNWIs to achieve a range of financial goals, including wealth preservation,” says Lee. “It provides a versatile tool to navigate uncertain markets and create a lasting legacy, offering HNWIs greater peace of mind.”

This material is intended to provide a general overview of Manulife Singapore’s insurance products. This material is for distribution in Singapore only and shall not be construed as an offer to sell or solicitation to buy or provision of any insurance product outside Singapore.

- https://www.ubs.com/global/en/family-office-uhnw/reports/global-wealth-report-2023/_jcr_content/pagehead/

- https://www.capgemini.com/news/press-releases/global-high-net-worth-population-sees-biggest-decline-in-size-and-wealth-for-over-a-decade/

- https://www.capgemini.com/news/press-releases/global-high-net-worth-population-and-wealth-back-to-record-levels-despite-global-instability/

- https://worldpopulationreview.com/country-rankings/richest-asian-countries

- https://www.fidelityinternational.com/editorial/article/asia-high-yield-is-not-just-china-now-6f825c-en5/

- https://www.weforum.org/agenda/2024/01/economic-outlook-2024-recession-inflation

- https://www.businesstimes.com.sg/companies-markets/banking-finance/interest-rates-fall-central-banks-are-no-longer-lock-step

- https://www.statista.com/outlook/tmo/cybersecurity/worldwide#:~:text=Revenue%20in%20the%20Cybersecurity%20market,US$271.90bn%20by%202029